.jpg)

Relative depreciation rates among different car makes and models is pretty trivial compared to the overall depreciation rate. A big gash, or a small cut, you are still bleeding to death.

In response to a my posting on "Never Co-Sign A Loan!" I got a note from a young man who defended asking his Mom to co-sign his loan on the grounds that "A new Honda or Toyota doesn't depreciate much, so buying a used one is not that great a deal!"

Sounds like something a car salesman said to him, doesn't it? And I know this, because I have heard this before - from car salesmen.

And recently, a reader wanted me to validate his decision to buy a brand new diesel car on the grounds that "the depreciation is less on a diesel!"

Sorry, no sale again, and again, something that a salesman would say, or your brain-dead friends who already bought and want to validate a poor choice they made.

Brand-new cars are a bad idea from the depreciation standpoint, for two reasons:

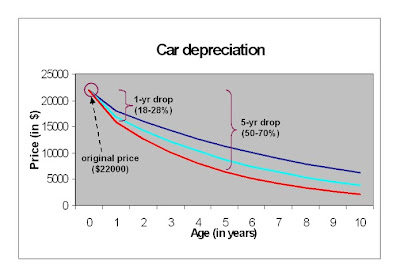

1. They depreciate rapidly, by 10% or more, the day you buy them.

2. Since they cost more, the dollar amount of depreciation is higher.

For example, my friend bought this nice Mercedes. Hardly a practical car, but it is a nice red coupe with a 300 HP engine and AMG package. A fun car, and only $17,000 with 58,000 miles on the clock. The original owner lost about $36,000 in depreciation to drive those 58,000 miles. My friend will drive it nearly as far, if not further, and lose a helluva lot less, in terms of depreciation. Perhaps $10,000 at most.

Yes the car will depreciate. But half of $17,000 is a lot less than half of $53,000. And the same analysis applies no matter what kind of car you are looking at, from econobox to hot rod - the analysis is the same. Cars depreciate, and the difference among them is trivial.

Or take my 2002 BMW X5. The original owner paid $53,000 for it, to drive it about 50,000 miles. I bought it for $25,000. The original owner paid about 50 cents a mile in depreciation. I've had it for eight years now - and 100,000 additional miles - and it is worth maybe $10,000 on a good day. My depreciation cost is about 15 cents a mile - far less than 50 cents. As I noted in my Actual Cost of Owning A Car posting, depreciation is a huge expense, and buying brand-new cars is one way to double or even triple your depreciation costs.

Yes, there are repair costs with owning an older car. But the depreciation expense the original owner paid ($28,000) far exceeds the repair costs I have incurred in nearly a decade and 100,000 miles of driving.

But what about cars with "low depreciation"? Sorry, but no sale. Even cars that "hold their value", such as a BMW, still depreciate rapidly. You are talking about losing tens of thousands of dollars in depreciation, even if the rate is as low as 40% every five years.

Yes, once in a great, great while, you find a car that is worth more after you bought it new. But that is not something you can count on. In early 1980's, when inflation was high, and Japanese cars were being sold for cheap, demand spiked, and many folks found, that for a brief year or so, you could buy a Honda Civic, drive it a year, and sell it for more than you paid for it.

But, like the price of gold, this did not last long, as people quickly realized that it was just a car, and moreover, Honda ramped up production to meet demand. Buying any commodity during a price spike or bubble is a bad idea - these are transient signals, not long-term trends.

So how much does depreciation vary? By not a lot, I am afraid. As in the gas mileage analysis, once you get beyond 20 mpg, the incremental savings drop off in a hurry. If you are getting gas mileage in the 30's, you are doing well, even at $5 a gallon. Going to the 40's, if it means buying a more expensive hybrid or paying more for fuel, is a wash - the payback is so small between 35 mpg and 45 mpg that the savings would take a decade or more.

And the same is true of depreciation. American cars have had the reputation of having the worst depreciation rates. But that does not mean they are twice as bad as a "good" car, only perhaps 50% worse. And part of this is - or was - due to the fact that American car makers have, historically, overpriced their "sticker" prices on their cars. So, in the past, a car with a $30,000 sticker price rarely left the showroom for over $25,000. And if you measure "depreciation" based on the sticker price alone, you would show a huge drop in value.

But part of it also was due to the perceived quality of American cars. And perhaps this will change - perhaps not. But the deal is, finding a car that "depreciates less" is not solving the problem, only improving it slightly.

For example, a 2007 Jetta sells for about ten grand, used. A new one can run from $16,000 to $25,000, depending on model. So, even though this may be a car with "low depreciation" it still drops by half, in value. A 2007 Chevy Cobalt runs a little less ($9000 or so) compared to its new Cruze replacement which runs $16,000 to $23,000.

So, the VW is a better deal because it "depreciates less" - right? Well, not exactly. While you might come out $1000 ahead buying the VW, used car prices are not an exact science (they do range based on condition). But moreover, you still end up losing about $6,000 to $10,000 in depreciation, over five years. This is a lot of money.

So a car with "low depreciation" still depreciates like a hemorrhaging femoral artery. The argument that a certain car is a "bargain" because of "low depreciation" is a specious argument.

But what about upgraded cars? Special edition units? High performance models? Same deal, different day. Such models cost more to buy, but they still depreciate along the same or similar curve. They are worth more later on, only because they cost more. So yes, a Jetta Diesel is worth more than a gas model, after a few years - but only because it cost more to begin with.

So why do people make these arguments? Well car dealers make them all the time. Go into a BMW showroom, and the salesman will tell you that since BMWs have a "low depreciation rate" that they can offer you a monthly lease with a low, low price. And it is a bit of a lie, because the lease rate is not that low, and it neglects to include the up-front costs (often in the thousands) as well as the back-end costs. Salesmen will say anything to make a sale.

Or take my young friend who wants his Mom to co-sign a loan on a brand-new Honda, when he is just age 22. He uses this depreciation argument (no doubt with his Mom) to just get what he wanted all along - a cool new car. Or at least what a young man thinks is a cool car.

And we all do this - all the time. It is human nature to justify decisions you have already made, and to try to distort logical arguments to justify emotional decisions.

For example, car repairs are often used as an emotional justification to buy a new car. "This old heap is costing me too much money! I should just trade it in on a brand-new one! For what I am paying in repairs, I could make the monthly payments on a new car!"

And if your car reaches the end of the Weibull curve, this may be true. But for a car reaching midlife that needs new tires and a timing belt, it may hardly be the case.

But even assuming your old heap needs a new transmission, and it is time to junk it, how does this rationalize going from one extreme (junker) to another (brand new car)? It doesn't of course, it is just a way we deceive our brains into justifying a "I want, gimme, gimme, gimme!" kind of decision.

The same is true of gas mileage arguments. Going from a 30 mpg car to a brand-new 40 mpg car might save a trivial amount of fuel, but won't save a lot of MONEY, which is the real key, unless you are being paid in gasoline these days. But people do this, taking on $25,000 in loan debt, on the premise that saving $250 a year on fuel makes it all worthwhile.

It is akin to the Captain of a sinking ship, who kicks aside the elderly, handicapped, and small children, so he can be the first on the lifeboat. When asked later on why he did this shameful thing, he says, "Well, I needed to be there to supervise the evacuation!" And maybe in his own mind, he starts to believe this.

But few others do.

The road to middle-class poverty is paved with new-car payments. And I know this, firsthand. I had a 1988 Toyota Camry, which was a nice car for its day, and in 1995, I decided to sell it, for more than half what I paid for it used in 1990 (it had "low depreciation", but still depreciated).

I paid $11,000 for the car, and it was worth $6500. It needed a timing belt, a new muffler, and a brake job. I paid about $800 to have this done, and used that rationalization to justify buying a new Taurus SHO for $25,000. "Better get rid of the Camry - it is getting old and unreliable!"

And yea, it was about as believable as the excuses proffered by the Captain of the Costal Concordia.

Was it a mistake? Yes. Because that Camry would easily have gone another 80,000 miles. And I know this because I sold it to a neighbor who did just that and never did a lick of work on it, other than to put gas in it and change the oil. Meanwhile, the SHO depreciated from $25,000 down to $8,000 (a much higher depreciation) after I spent several thousand dollars having work done on it.

I could have simply skipped a car, and come out well over $30,000 ahead. Is that a lot of money? You bet it is - even if you are a Millionaire.

The best used car value is often parked in your driveway. And you should think about this, before you trot off to the dealer to be seduced by shiny paint and a built-in GPS.

And this posting is timely, as car sales have rocketed in recent months. After three years of lackluster sales, many people are reacting to "pent-up demand" and trading in their cars. The lack of off-lease cars from the 2009 era means that even used cars are in short supply, and the tsunami has shortened the supply line of Japanese cars.

Does this mean there is a "car shortage"? Hardly. Small changes in supply and demand can result in HUGE swings in price. So a 5% increase in buyers and a 5% decrease in supply means that prices jump 10% or more.

And by the way, that is another post hoc rationalization people use to buy brand-new cars these days. "Well, used car prices are so high right now! I'll get a better trade-in on my used car!"

Funny. Where did I hear that argument before? Oh, yea, Fort Lauderdale, Florida, circa 2005. Only it was with regard to houses, not cars.

How did that work out?

If you want to buy a new car, go knock yourself out. But just break down and admit to yourself you are doing it for emotional, not logical reasons. Trying to trot out the same tired old arguments, distorting logic to justify emotions, is just, well, embarrassing. And if you go down this road, pretty soon you will be getting 500 channels of cable because "it is our only luxury, and cheaper than going to a movie" or a $100-a-month smart phone, so you can "stay in touch with the grandkids."

Go ahead. Knock yourself out. But don't forget about your net worth, your retirement, and your life down the road. A brand-new car is never a "bargain" when you add up the overall transaction costs.

0 comments:

Post a Comment